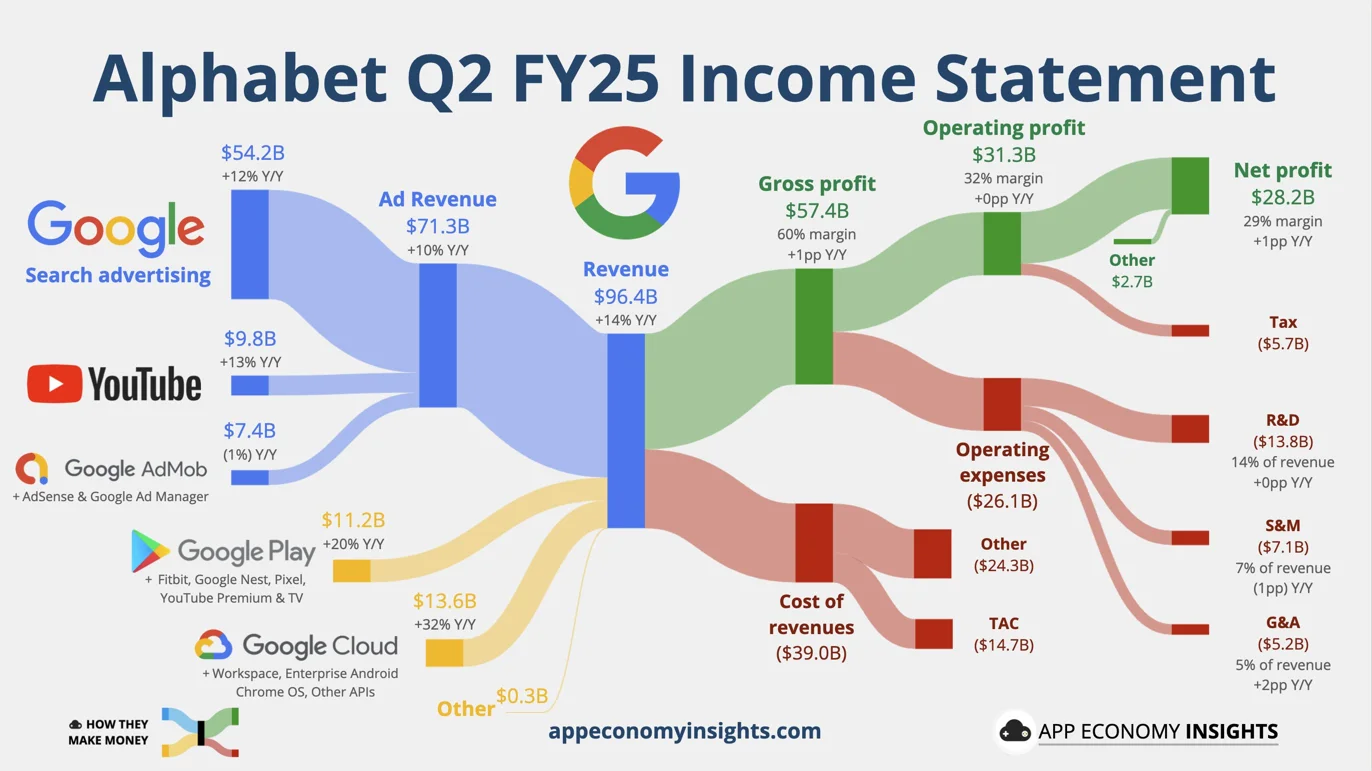

Alphabet's Q2 FY25 results showed strong performance with revenue up 14% year-over-year to $96.43 billion, beating estimates by $2.5 billion. The operating margin remained steady at 32%, and EPS was $2.31, beating expectations by $0.12. The company’s shares rose up to 3% in after-hours trading.

Key Business Segments

- Google Cloud revenue surged 32% to $13.62 billion, surpassing estimates, with operating margin improving by 9 percentage points to 21%. This growth is driven by strong demand and partnerships, including OpenAI's use of Google Cloud for ChatGPT.

- YouTube advertising revenue increased 13% to $9.8 billion, exceeding analyst expectations.

- The search unit generated $54.19 billion, contributing to total advertising revenue of $71.34 billion, up about 10.4% from the previous year.

- The “Other Bets” segment, including Waymo and Verily, brought in $373 million in revenue but reported a loss of $1.25 billion, higher than the previous year’s loss.

Financial Highlights and Investments

- Alphabet’s net income rose nearly 20% to $28.20 billion.

- The company announced a significant increase in capital expenditures for 2025 to $85 billion, up from the previously expected $75 billion, driven by expanding AI and Cloud investments. Further increases are expected in 2026.

- Traffic acquisition costs (TAC) were $14.71 billion, slightly above estimates.

- Total operating expenses rose 20% to $26.1 billion, largely due to legal and settlement costs, including a $1.4 billion charge related to a $1.37 billion settlement with Texas over a 2022 data privacy lawsuit.

AI and User Growth

- Google’s AI search product, AI Overviews, now has over 2 billion monthly users, up from 1.5 billion last quarter.

- The Gemini app, featuring Alphabet’s AI chatbot, has surpassed 450 million monthly active users.

- Alphabet is investing heavily in AI talent, exemplified by a $2.4 billion deal to acquire top researchers and technology from the AI coding startup Windsurf.

Outlook

- Alphabet’s finance chief Anat Ashkenazi indicated potential revenue tailwinds in Q3, partly due to strong advertising spend linked to the 2024 U.S. elections, especially on YouTube.

- Despite rising competition in AI, Alphabet’s search and advertising businesses continue to grow steadily, supported by ongoing investments in AI and cloud infrastructure.